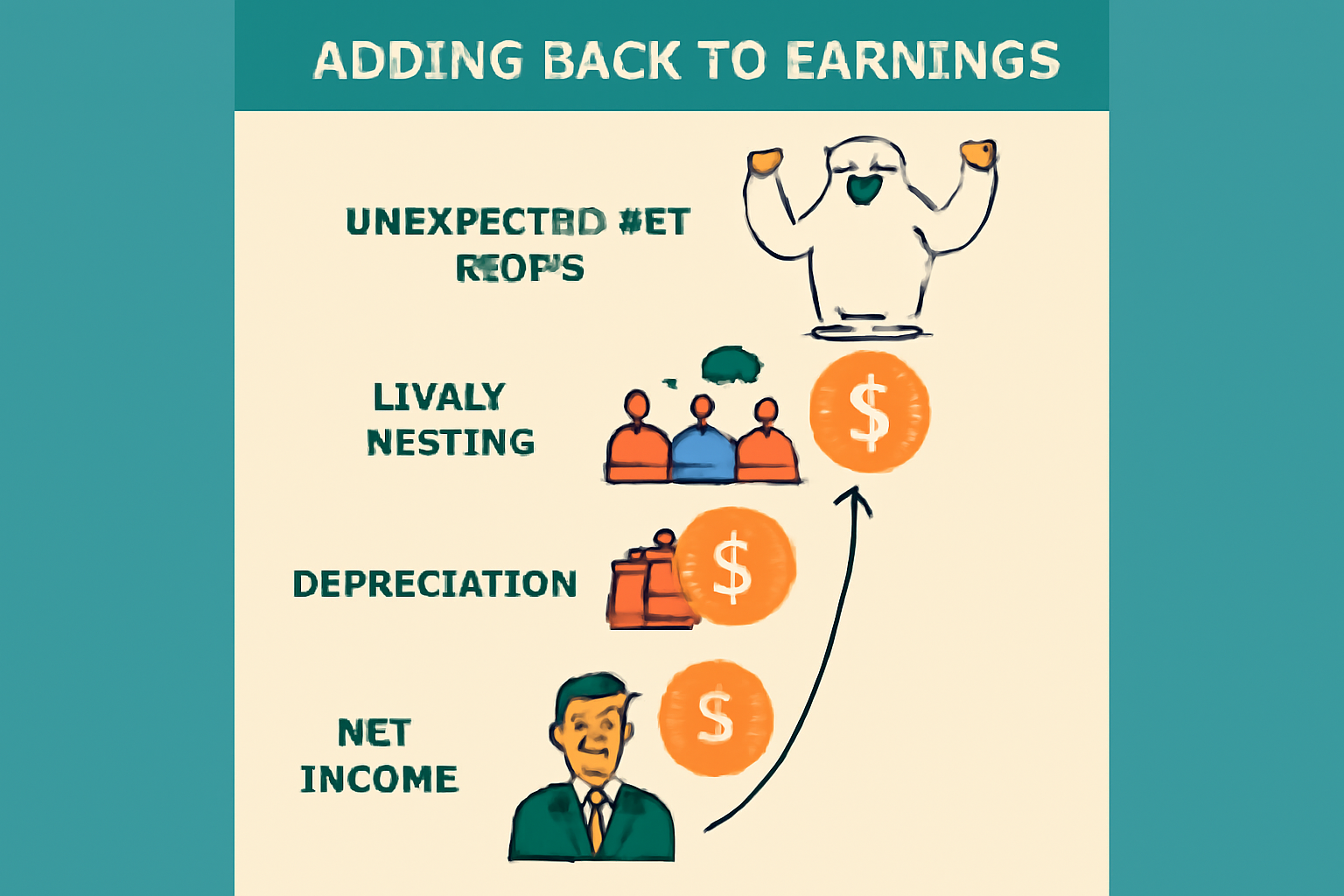

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) add-backs are adjustments made during financial statement analysis to provide a clearer picture of a company's recurring earnings. These adjustments are critical for investment evaluations, mergers and acquisitions, and lending considerations. However, as financial scrutiny intensifies and competitive pressures mount, companies are employing increasingly creative strategies to expand these add-backs.

Non-Recurring Expenses: Traditional add-backs have included items like litigation costs, restructuring expenses, and one-time management bonuses. Companies are now extending this to include costs from aborted transactions and fluctuations in foreign exchange rates, arguing that these are not reflective of ongoing operations.

Startup Costs: With rapid technological advances and startup growth, early-stage businesses are frequently including all manner of developmental costs. This might cover R&D expenses or significant customer acquisition costs, asserting these investments are foundational and not recurrent operational costs.

Regulatory Costs: With evolving compliance landscapes, enterprises claim add-backs due to unexpected, new regulatory compliance costs which they argue distort the financial performance but are crucial to understand the normal earning power.

COVID-19 Related Costs: More recently, COVID-19 has provided a broad umbrella under which many costs have been categorized as extraordinary. This expansive categorization aims to isolate the financial impact from regular failing business performance.

Synergies and Efficiencies: Anticipated synergies from acquisitions or internal efficiencies yet to be realized are being preemptively added back to EBITDA, although their eventual realization is uncertain.

Non-Cash Expenses: More companies are adding back non-cash expenses like stock-based compensation, although this can potentially overstate available cash flow.

It is vital for analysts and investors to maintain a critical perspective on these adjustments, ensuring they are truly non-recurring or non-operational. Rigorous due diligence involves scrutinizing each add-back to gauge its legitimacy and effect on the accurate depiction of earning sustainability. Over-aggressive add-backs can obscure true financial health and lead to misinformed decisions.